Estate planning strategies help support early retirement by protecting assets, reducing risk, and keeping your finances organized over time.

Retiring early means relying on your assets for decades. This increases exposure to taxes, health care costs, and changing financial needs. Without coordination, gaps can lead to losses or disruptions.

What helps keep everything stable over that kind of timeline? Keeping your plan aligned helps reduce risk and maintain consistency.

The following strategies outline how to protect your assets and maintain stability throughout early retirement.

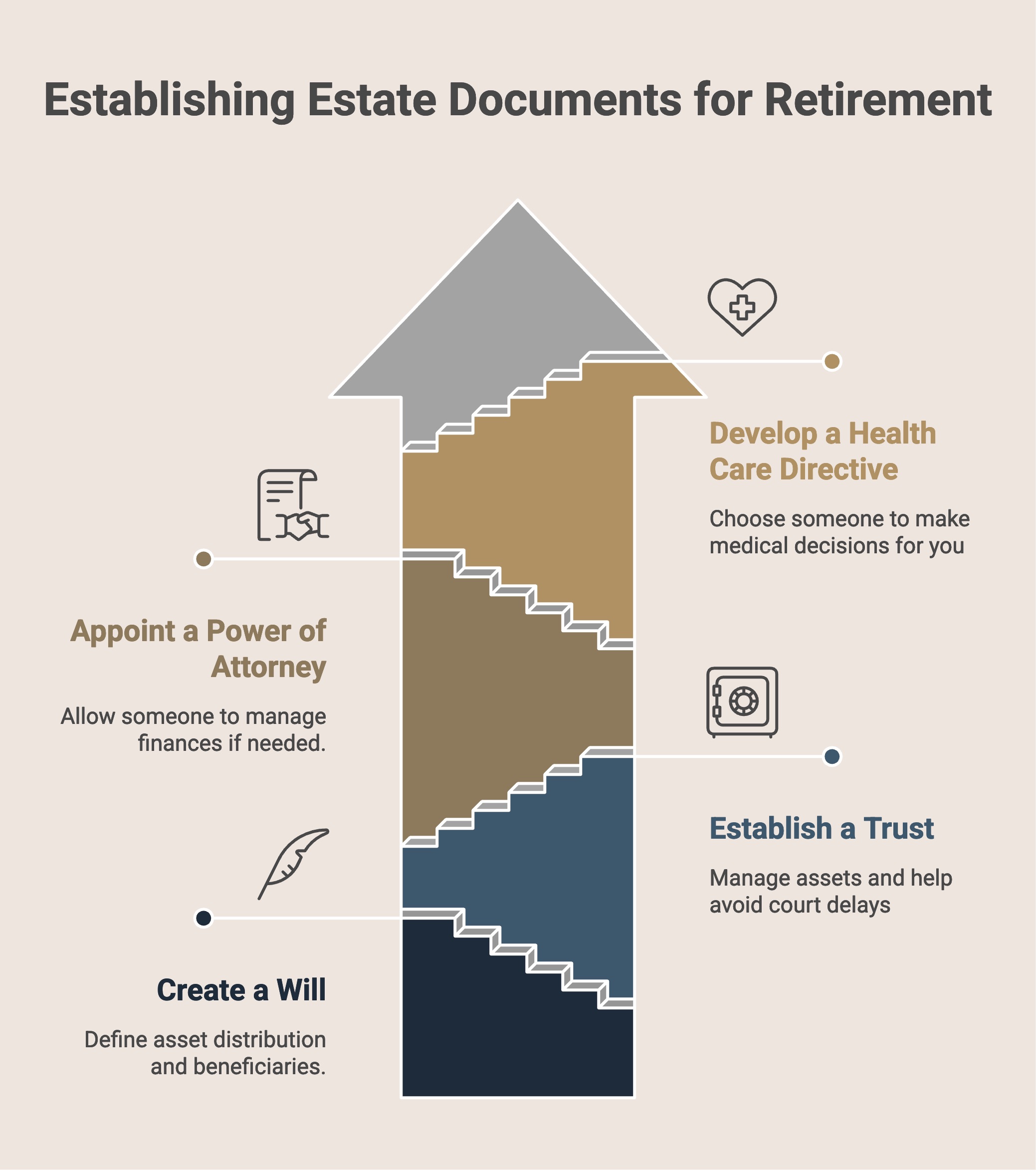

1. Start with the estate documents you still need

Start by putting core estate documents in place early, since they set the foundation for how your assets and decisions are handled throughout retirement.

Focus on completing:

- A will to define how your assets are distributed

- A trust to manage assets and help avoid probate

- A durable financial power of attorney (POA) to allow someone to manage finances if needed

- A health care power of attorney (HCPOA) to guide medical decisions and assign authority

This strategy helps prevent delays, avoids court involvement, and keeps decision-making in trusted hands. For early retirement, having these documents in place supports a longer timeline where your plan needs to function without interruption.

2. Review assets, titles, and beneficiaries early

Review how your assets are owned and who is listed as a beneficiary. These details control how property transfers during retirement.

Create a clear list of major assets, including retirement accounts, insurance policies, real estate, and investment accounts. Check how each asset is titled and who is named as the beneficiary, since these details determine who receives them, not just your will.

Align ownership with your plan. For example, assets intended for a trust should be retitled in the name of the trust, and beneficiary designations should match your current wishes.

Update outdated designations after life changes such as marriage, divorce, or the birth of a child. Even one outdated name can override your entire plan.

Keeping these details updated helps your plan stay clear, directs assets to the right people, and reduces the risk of delays or confusion during retirement.

3. Use trusts to protect more and avoid delays

Use trusts to control how assets are managed and passed on while reducing delays in the transfer process. Different types of trusts and related approaches serve specific purposes depending on how you want assets handled:

- Revocable living trust: Allows assets to pass without going through probate, helping avoid delays

- Irrevocable trust: Moves assets out of your taxable estate, which may reduce future tax exposure

- Annual gifting: Allows transfers of up to $19,000 per person in 2026, gradually reducing estate size

- Structured distributions: Releases assets over time instead of all at once, helping manage spending

4. Plan for health care and incapacity costs

Set up a plan that covers both medical decisions and how care will be paid, since early retirement increases the years you may rely on these arrangements.

Use legal documents to assign decision-making authority and outline your medical preferences so actions can be taken without delay. At the same time, review how care costs will be funded, including savings, insurance, or asset protection structures.

Long-term care can exceed $90,000 per year, so planning for this early protect retirement savings and prevents forced asset liquidation later.

5. Coordinate taxes with your retirement plan

Tax planning affects how much of your savings you keep during retirement. Use a structured approach to manage how income is taxed over time:

- Tax-deferred strategies: Delay when income is taxed, then plan withdrawals to manage how much income is taxed during retirement

- Roth accounts: Allow qualified withdrawals without income tax, which can reduce tax exposure later and provide flexibility in managing income

- Withdrawal timing: Spread withdrawals across different account types to avoid pushing income into higher tax brackets

- Gifting strategy: Use annual limits of $19,000 per person in 2025 to gradually reduce your taxable estate

Estate planning also supports tax efficiency in how assets are transferred. Coordinating timing, ownership, and distribution methods reduce unnecessary tax impact and keeps more of your assets available to support early retirement.

6. Protect business, property, and complex assets

Create a structure that separates, protects, and controls high-value assets so they continue to support your retirement without unnecessary risk.

Separate personal assets from business or property risks. For example, holding rental properties or business interests in a legal structure can help limit how much you are personally exposed if issues come up.

Use trusts to control and protect certain assets. Some trust structures can move assets out of your estate or protect them from claims, while still allowing planned use over time.

Add another layer of protection with insurance. Higher coverage can help protect against large claims, especially if you own property or run a business.

When these pieces are set up correctly, your assets are more protected, easier to manage, and better able to support your retirement over a longer period.

7. Update your plan as retirement goals change

Update your estate plan regularly so it stays aligned with your retirement goals and timeline.

Early retirement can last 30 years or more, which means your needs will change over time. Spending patterns, income sources, and health care costs may shift, so your plan should reflect those changes.

Review how much you withdraw each year and adjust if needed to avoid putting pressure on your savings. Revisit your target savings and expenses to confirm they still match your lifestyle.

Keeping your plan updated helps your assets last longer and supports more stable decision-making throughout retirement.

Protect your early retirement with the right plan

A well-structured plan helps protect what you have built and keeps your retirement steady over time.

Working with an experienced estate planning attorney gives you guidance across business, tax, and asset protection, along with ongoing updates as your situation changes. Local insight in Colorado keeps everything practical and aligned with your goals.

For your early retirement plans, having everything set up correctly can make a meaningful difference. Book a free consultation today.

Frequently asked questions

What is the biggest mistake most people make regarding retirement?

Underestimating how long retirement lasts is the biggest mistake. Many plans fail because they ignore inflation, taxes, and rising health care costs in the long run.

Who should I not name as a beneficiary?

Avoid naming minors, your estate, or someone financially unprepared without a structure. These choices can lead to delays, court involvement, or poor management of assets.

What are the disadvantages of putting your house in an irrevocable trust?

You give up direct control of the property once it is transferred. Changes like selling or refinancing may require approval and can limit flexibility.

Do beneficiaries pay tax on capital gains?

Yes, but only on gains after the asset is inherited. Most assets receive a step-up in basis, which reduces the taxable amount at the time of transfer.

How often should you update your estate plan in retirement?

Review your plan every two to three years or after major life changes. Regular updates keep documents, beneficiaries, and asset instructions aligned with your current situation.

0 Comments