Estate planning helps organize how assets are managed, who can make decisions, and how property is passed on over time. When done well, it brings structure and reduces uncertainty for the people involved.

The right estate planning strategies depend on life stage and financial circumstances. Some address incapacity, others focus on efficient transfers, tax considerations, or long-term family continuity. Knowing which tools apply, and when, keeps planning manageable rather than overwhelming.

This article outlines 10 estate planning strategies, drawn from work with individuals and families, and explains how each one supports stability and continuity over time.

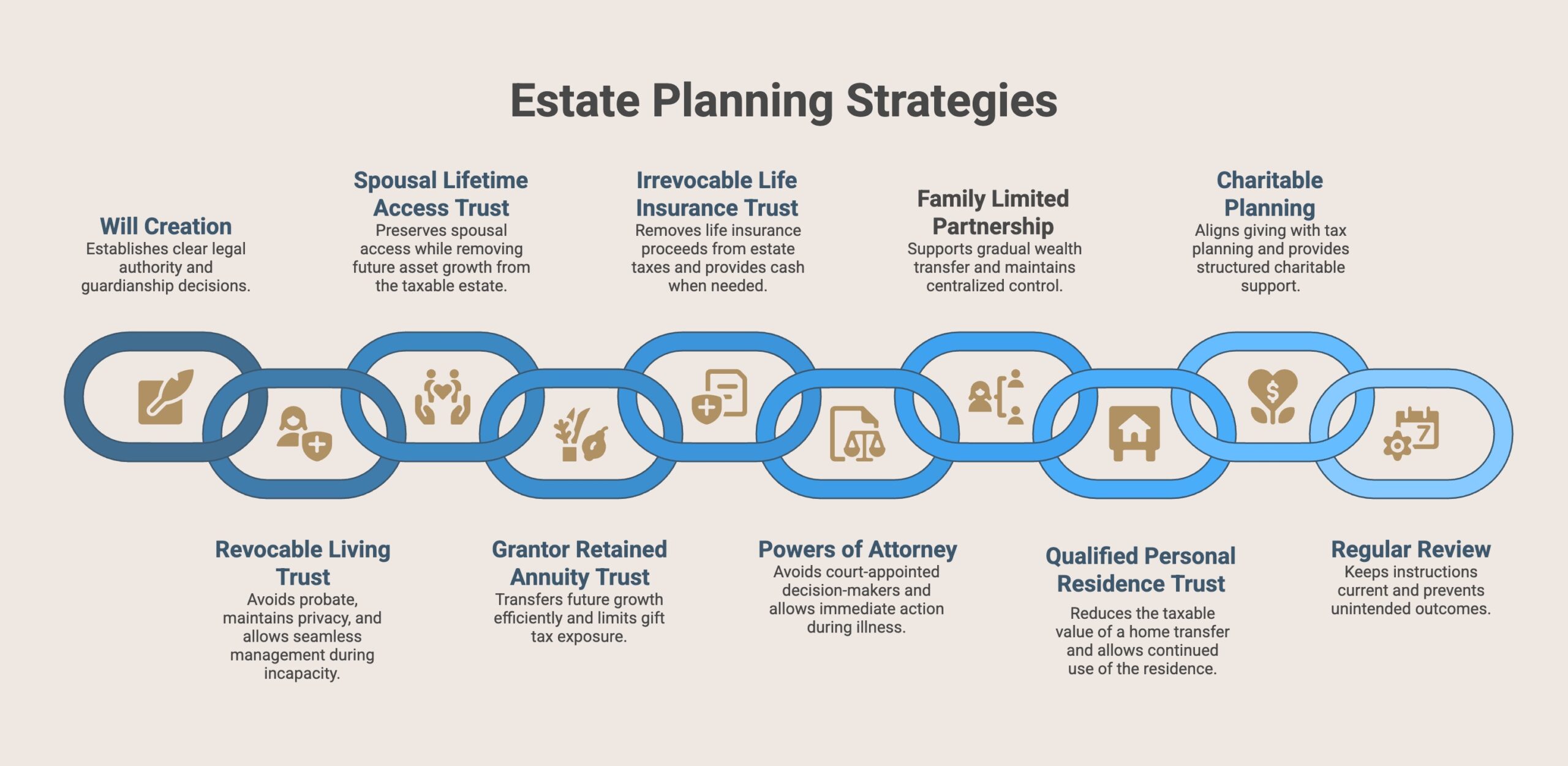

1. Create or Update Your Will

A will is the starting point for directing what happens after death. It defines who receives assets, who is responsible for administration, and who will care for minor children.

According to legal experts, a will also appoints an executor to collect assets, pay debts, and distribute the estate according to the instructions provided.

Without a current will, state law controls these decisions, which may not reflect family priorities or relationships. Reviewing and updating a will after major life changes helps keep instructions aligned with current circumstances.

Why this strategy matters:

- Establishes clear legal authority

- Confirms guardianship decisions

- Prevents default state rules from applying

2. Establish a Revocable Living Trust

A revocable living trust is used to manage and transfer assets without court involvement. The strategy focuses on continuity, privacy, and timing rather than ownership alone.

Assets placed in the trust can be managed during incapacity and transferred after death without probate. This allows beneficiaries to access assets more efficiently and reduces administrative delays.

Why this strategy matters:

- Avoids probate and court oversight

- Maintains privacy

- Allows seamless management during incapacity

3. Use Spousal Lifetime Access Trusts (SLATs)

A Spousal Lifetime Access Trust allows married couples to move assets out of their taxable estate while still keeping access to those assets during their lifetime.

One spouse places assets into the trust, and the other spouse can receive benefits from it, providing flexibility alongside long-term planning.

This strategy is often used to lock in available gift and estate tax exemptions while maintaining flexibility if financial needs change.

Why this strategy matters:

- Removes future asset growth from the taxable estate

- Preserves spousal access during life

- Supports long-term planning for children and grandchildren

4. Use Grantor Retained Annuity Trusts (GRATs)

A Grantor Retained Annuity Trust lets someone pass on assets that are expected to grow in value while keeping gift taxes low.

The person who creates the trust receives set payments for a fixed period, and any growth beyond that amount goes to the beneficiaries.

According to research, this structure allows future asset appreciation to transfer with little or no gift or estate tax impact. This strategy is commonly used for assets expected to grow in value, such as investments or business interests.

Why this strategy matters:

- Transfers future growth efficiently

- Limits gift tax exposure

- Works well for short-term planning around high-growth assets

5. Use an Irrevocable Life Insurance Trust (ILIT)

An Irrevocable Life Insurance Trust is used to keep life insurance proceeds outside of the taxable estate. The trust owns the policy, and benefits are paid directly to beneficiaries.

This strategy is often used to provide liquidity for taxes, debts, or expenses without forcing the sale of family assets.

Why this strategy matters:

- Removes life insurance proceeds from estate taxes

- Provides cash when it is needed most

- Protects proceeds from creditors and mismanagement

6. Designate Powers of Attorney for Property and Personal Care

This strategy is about preserving control during incapacity. Powers of attorney allow trusted individuals to manage finances and make healthcare decisions if you are unable to act.

Without these designations, a court may need to appoint someone, which can delay decisions and limit flexibility. Naming backups and reviewing these roles in advance helps ensure continuity.

Why this strategy matters:

- Avoids court-appointed decision-makers

- Allows immediate action during illness or injury

- Reduces stress for family members

7. Use a Family Limited Partnership or LLC

Family entities are used to keep management centralized while gradually passing ownership to the next generation. Interests can be transferred over time, while day-to-day control stays with the people chosen to run the assets or business.

This strategy is commonly used for family businesses, rental properties, or shared investments.

Why this strategy matters:

- Supports gradual wealth transfer

- Maintains centralized control

- Can reduce estate tax exposure

8. Use a Qualified Personal Residence Trust (QPRT)

A QPRT is used to transfer a primary or vacation home to heirs at a reduced gift value while allowing continued use of the property for a set period.

This strategy is most effective when long-term ownership transfer is planned and the owner expects to remain in the home for several years.

Why this strategy matters:

- Reduces the taxable value of a home transfer

- Allows continued use of the residence

- Moves future appreciation out of the estate

9. Incorporate Charitable Planning

Charitable planning strategies allow families to support causes they care about while addressing tax and income planning goals. Certain structures provide current tax benefits, ongoing income, or future charitable gifts.

This approach is often used when philanthropy is part of a broader legacy plan.

Why this strategy matters:

- Aligns giving with tax planning

- Provides structured charitable support

- Integrates values into long-term planning

10. Review and Update the Plan Regularly

Even well-designed plans require regular review. Life events, asset changes, and legal updates can affect how strategies function over time. Scheduled reviews with an estate planning attorney help ensure documents remain aligned with current goals and circumstances.

Why this strategy matters:

- Keeps instructions current

- Prevents unintended outcomes

- Allows timely adjustments as laws and families change

Where Planning Becomes Protection

Estate planning works best when it is intentional, coordinated, and revisited over time. The goal is not to use every available tool, but to apply the right ones based on your assets, family structure, and long-term priorities.

These estate planning strategies provide a framework for protecting assets, assigning authority, and guiding transitions with clarity. When addressed early and reviewed regularly, they reduce uncertainty and help ensure decisions are carried out as intended.

If you would like guidance reviewing your current plan or identifying which strategies are appropriate for your situation, contact us today to discuss next steps.

Frequently Asked Questions

Which estate planning strategies are most important to start with?

The most important starting strategies focus on authority and continuity. These usually include a will, powers of attorney, and basic coordination of assets. These tools establish who can act, how decisions are made, and what happens first, forming a foundation that more advanced strategies can build upon.

Do I need trusts if I already have a will?

In many cases, yes. A will sets direction after death, but trusts are often used to control timing, reduce court involvement, and manage assets during incapacity. The use of a trust depends on asset types, privacy concerns, and the level of structure needed for beneficiaries.

How do estate planning strategies change as assets grow?

As assets increase, planning often shifts toward tax efficiency, long-term control, and multigenerational continuity. Strategies may expand to include advanced trusts, business entities, or charitable planning. The focus moves from basic direction to preserving value and coordinating transfers over a longer time horizon.

Are estate planning strategies different for blended families?

Yes. Blended families often require additional planning to balance the needs of a surviving spouse and children from prior relationships. Specific strategies help clarify access, income rights, and final distribution to avoid unintended disinheritance or conflict between family members.

Why is regular review part of an estate planning strategy?

Estate planning strategies depend on current laws, assets, and family circumstances. Changes in life events or regulations can affect how a plan functions. Regular reviews help ensure strategies remain aligned with goals and continue to work as intended over time.

0 Comments