Helping a child with a home purchase or contributing to a grandchild’s education is a common way families support each other. When larger gifts are involved, an important question often follows. Do these transfers trigger gift taxes?

Understanding what are gift taxes helps families give with clarity and confidence. Federal gift tax rules track certain transfers of money or property, but generous exclusions and lifetime limits mean most family gifts never result in tax.

At Birch Grove Legal, estate planning often includes reviewing lifetime gifts and how they fit within long-term wealth planning. This article explains how gift taxes work, who is responsible for reporting them, and when the rules actually apply.

What Are Gift Taxes?

A gift tax is a federal tax that can apply when someone gives money or property and receives nothing of equal value in return. The person making the gift is called the donor. Gifts can include cash, real estate, investments, or even forgiving a loan.

Not every gift triggers tax rules. Small everyday gifts usually fall outside reporting requirements. Larger transfers, such as helping a child start a business or transferring valuable assets, may need to be reported to the IRS.

Gift taxes are part of the same system that governs estate taxes. Gifts made during your lifetime count toward a larger lifetime limit that also applies to your estate later. This structure prevents large estates from avoiding tax simply by giving assets away before death.

Federal gift tax rates currently range from 18% to 40%. In practice, most families never pay gift tax because the law provides generous annual exclusions and lifetime limits.

For example, transferring $50,000 in stock to a child is considered a gift because no value is received in return. The transfer may need to be reported on IRS Form 709. In most situations, however, no tax is owed if the gift falls within the available exclusions or lifetime exemption.

Who Pays Gift Taxes?

Gift tax responsibility falls on the person who makes the gift. The donor is responsible for reporting the transfer and filing any required forms with the IRS. The person receiving the gift does not pay tax on the gift itself.

If you give money, property, or other assets, you are the one responsible for tracking the amount and applying any available exclusions. When a gift exceeds the annual exclusion, the transfer is reported using IRS Form 709, which is typically filed by April 15 of the following year.

Filing a gift tax return does not automatically mean tax is owed. In many cases, the reported amount simply counts toward the donor’s lifetime gift and estate tax exemption.

Gift Splitting For Married Couples

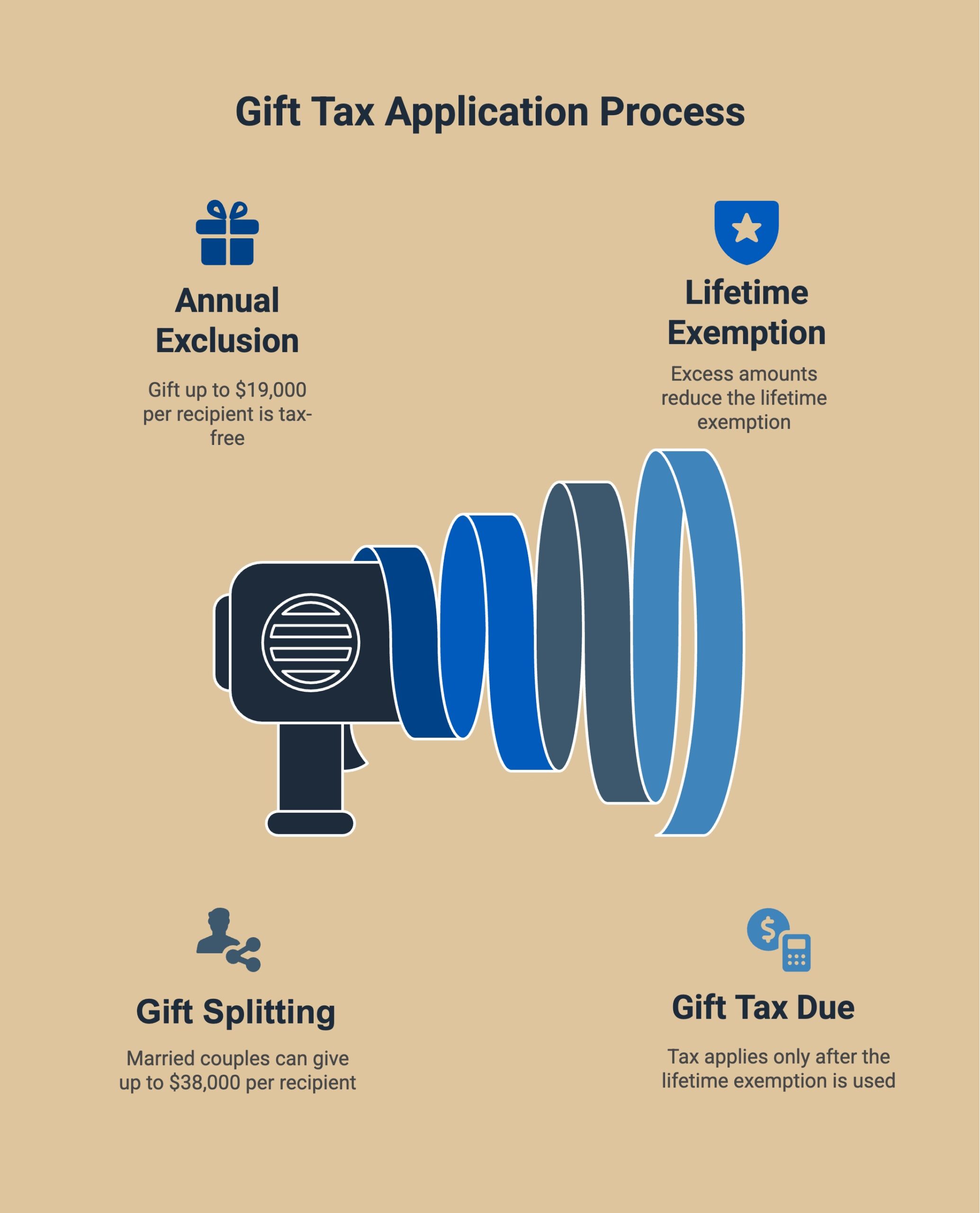

Married couples can also use a rule called gift splitting. This allows spouses to treat a gift as if each person gave half of the total amount. Doing this can effectively double the amount that can be given under the annual exclusion.

For example, if one spouse gives $30,000 to a child, the couple can elect to split the gift. Each spouse would report $15,000, which may remain within the annual exclusion depending on the year’s limits.

This structure allows families to transfer support while keeping gifts within the available rules.

When Do Gift Taxes Actually Apply?

Gift taxes do not apply to every transfer of money or property. The rules begin to matter only after a gift exceeds the annual exclusion and starts using the lifetime exemption.

For 2026, the annual exclusion allows someone to give up to $19,000 per recipient without affecting the lifetime limit. Married couples can combine their exclusions through gift splitting, allowing $38,000 per recipient in the same year. These limits apply separately to each person receiving a gift.

If a gift goes above the annual exclusion, the excess amount counts toward the lifetime gift and estate tax exemption. Gift tax only becomes due after the lifetime exemption has been fully used.

The rules work in a clear sequence:

- Annual exclusion applies first

- Excess amounts reduce the lifetime exemption

- Gift tax applies only after the exemption is fully used

Common Exemptions And Exclusions

Several exemptions allow gifts to pass without creating gift tax obligations. These rules help families support education, healthcare, and spouses while keeping transfers outside the gift tax system.

Gifts To A U.S. Citizen Spouse

Transfers between spouses who are U.S. citizens are generally unlimited. These gifts do not require reporting and are not subject to gift tax.

Direct Tuition Payments

Tuition payments made directly to a school are not treated as taxable gifts. The payment must go straight to the educational institution for the exclusion to apply.

Direct Medical Payments

Medical expenses paid directly to a healthcare provider are also excluded from gift tax rules. This can include payments for treatment, procedures, or medical insurance premiums.

Charitable Contributions

Gifts made to qualified charitable organizations are fully deductible and are not treated as taxable gifts under federal law.

Gifts To A Non-Citizen Spouse

Different rules apply when the receiving spouse is not a U.S. citizen. In 2026, the annual exclusion for gifts to a non-citizen spouse is $194,000.

These exemptions allow families to provide meaningful support without affecting the annual exclusion or lifetime exemption. An estate planning attorney can help review how these exclusions apply to your situation and ensure gifts are structured correctly within a broader estate plan.

Review Your Gifting Plan With Birch Grove Legal

Gift tax rules exist to track large transfers of wealth, but federal law also provides generous exclusions that allow families to give within clear limits. Annual exclusions, lifetime exemptions, and specific exceptions for education and medical expenses allow many financial gifts to pass without creating tax.

Knowing what are gift taxes and how the rules apply helps families coordinate lifetime gifts with broader estate planning goals. A clear strategy keeps transfers properly documented while preserving flexibility for future planning.

If you are considering larger gifts or want to review how past transfers affect your estate plan, contact us today to speak with Birch Grove Legal about the next steps.

Frequently Asked Questions

Do I Have To Pay Gift Tax When I Give Someone Money?

Most gifts do not result in gift tax. In 2026, individuals can give up to $19,000 per recipient each year without filing a gift tax return. Married couples can combine exclusions and give $38,000 per recipient. Gifts above that amount must be reported, but tax usually does not apply unless lifetime limits are exceeded.

What Is The Gift Tax Annual Exclusion?

The annual gift tax exclusion is the amount someone can give to another person each year without filing a gift tax return. For 2026, the exclusion is $19,000 per recipient. The limit applies separately to each recipient, allowing gifts to multiple individuals during the same year without reporting.

When Do I Need To File A Gift Tax Return?

A gift tax return must be filed when a gift exceeds the annual exclusion amount. The donor files IRS Form 709 to report the excess portion of the transfer. Filing the return records the use of the lifetime gift and estate tax exemption and does not automatically create a tax payment.

Are Tuition And Medical Payments Subject To Gift Tax?

Tuition and medical payments are excluded from gift tax when paid directly to the educational institution or healthcare provider. These payments do not count toward the annual exclusion or the lifetime exemption. If the money is given to the student or patient instead, normal gift tax rules apply.

What Happens If A Gift Exceeds The Annual Exclusion?

When a gift exceeds the annual exclusion, the excess amount is applied to the donor’s lifetime gift and estate tax exemption. For 2026, the exemption is $15 million per individual. Gift tax is owed only after that lifetime exemption has been fully used. Until then, the gift is reported but not taxed.

0 Comments